A lot of people start in the same place. They have an insurance card, a real need for therapy or addiction treatment, and almost no confidence that the plan will pay for care. The language on the back of the card feels technical, the member portal is full of vague labels, and every answer seems to lead to three more questions.

That confusion intensifies when the need is urgent. Someone may be trying to find counseling for anxiety, verify coverage for outpatient addiction treatment, or understand whether a residential program is covered at all. The phrase therapy covered by medical sounds simple, but the actual answer depends on medical necessity, diagnosis, network rules, and how the facility bills treatment.

Navigating the Maze of Mental Health Insurance

A patient calls for help after weeks of putting it off. Within minutes, the conversation turns from symptoms to insurance terms like PPO, deductible, out-of-network reimbursement, preauthorization, and medical necessity. For many people, that is the moment treatment starts to feel harder than it should.

The confusion is real because coverage is rarely a simple yes or no. A plan may cover therapy, outpatient treatment, or even residential care, but the actual result depends on how the insurer classifies the service, whether the provider is in network, and what records are needed before approval. Patients often assume the insurance card gives them a clear answer. In practice, the card is only the starting point.

Access gets harder when a higher level of care is involved. Residential addiction treatment, dual diagnosis care, and luxury rehab settings often raise extra questions about authorization, reimbursement, and what portion of the stay the plan will recognize as medically necessary. Learning how insurance works for luxury rehab helps patients ask better questions before they commit to a program.

The actual trade-off is time versus clarity.

Some families try to decode the policy on their own, call the insurer, then call providers one by one. That can work, but it often leads to partial answers because the insurance company explains benefits in general terms while the treatment center has to match those benefits to a specific clinical recommendation and billing structure. A strong admissions team closes that gap by verifying benefits, identifying likely out-of-pocket costs, and explaining what still needs insurer review.

That process also depends on privacy and accurate communication. Many treatment programs rely on secure intake systems and protected patient calls, which is one reason operational standards like building a HIPAA compliant call center matter behind the scenes.

Patients do not need to become insurance experts before asking for help. They do need a clear verification process, honest answers about limits, and a treatment team that can explain what the plan is likely to cover before admission.

The Legal Foundation for Your Mental Health Coverage

A patient calls for help, asks whether therapy is covered, and gets an answer that sounds promising but incomplete. The plan covers behavioral health. Authorization may apply. Out-of-network benefits may exist. For someone already dealing with anxiety, depression, trauma, or substance use, that answer rarely brings relief. It usually creates more questions.

Federal law gives that conversation a clearer starting point. Mental health treatment is part of medical care under many health plans, and patients have legal protections before anyone starts debating copays, authorizations, or claim forms.

What the ACA requires

The Affordable Care Act requires many ACA-compliant plans to include mental health and substance use disorder services as essential health benefits. In practical terms, therapy, psychiatric care, and addiction treatment are not supposed to be treated like optional extras in those plans.

That does not mean every service is covered in every setting. Plans still apply medical necessity rules, network rules, and plan-specific exclusions. The law sets the floor. The policy details still control what happens when a patient seeks care.

This distinction matters for families comparing outpatient therapy, intensive programs, or residential treatment. The legal question is often already settled. The essential question is whether the plan recognizes the recommended level of care for that patient’s clinical needs.

What parity means in everyday language

The Mental Health Parity and Addiction Equity Act requires many insurers to apply mental health and substance use benefits in a way that is comparable to medical and surgical benefits. If a plan uses prior authorization, visit limits, or cost-sharing rules more aggressively for behavioral health than for similar medical care, that can raise parity concerns.

Patients do not need to cite federal statutes on the phone with an insurer. They do need to know that therapy and addiction treatment are protected categories of care under federal law, not fringe benefits the plan can restrict however it wants.

That legal protection helps, but it does not answer the practical questions families ask during admissions.

Why privacy matters during verification

Insurance verification often requires discussion of diagnoses, prior treatment, medications, relapse history, and family concerns. Those conversations need to be handled carefully and securely, especially when a treatment center is coordinating benefits review and clinical intake at the same time.

That is one reason strong admissions operations rely on protected systems and trained staff. For a practical example of how healthcare organizations support private intake communication, see this guide to building a HIPAA compliant call center.

What this means for someone seeking care

Patients already have a legal foundation for mental health coverage. The hard part is turning that legal protection into a clear yes, no, or partial answer for a specific program.

A useful verification review should answer four points:

- Which services the plan recognizes: therapy, psychiatry, substance use treatment, and higher levels of behavioral health care

- Which setting may be covered: outpatient, intensive outpatient, partial hospitalization, detox, or residential treatment

- Which financial rules apply: deductible, copay, coinsurance, out-of-pocket maximum, and any separate out-of-network exposure

- Which insurer approvals are still pending: prior authorization, concurrent review, or additional medical records

This is why many patients start confused and only get clarity after a treatment center reviews the policy against actual clinical recommendations. At Oceans Luxury Rehab, that verification process is not a side task. It is part of helping patients understand what the law promises, what the plan covers, and what steps come next.

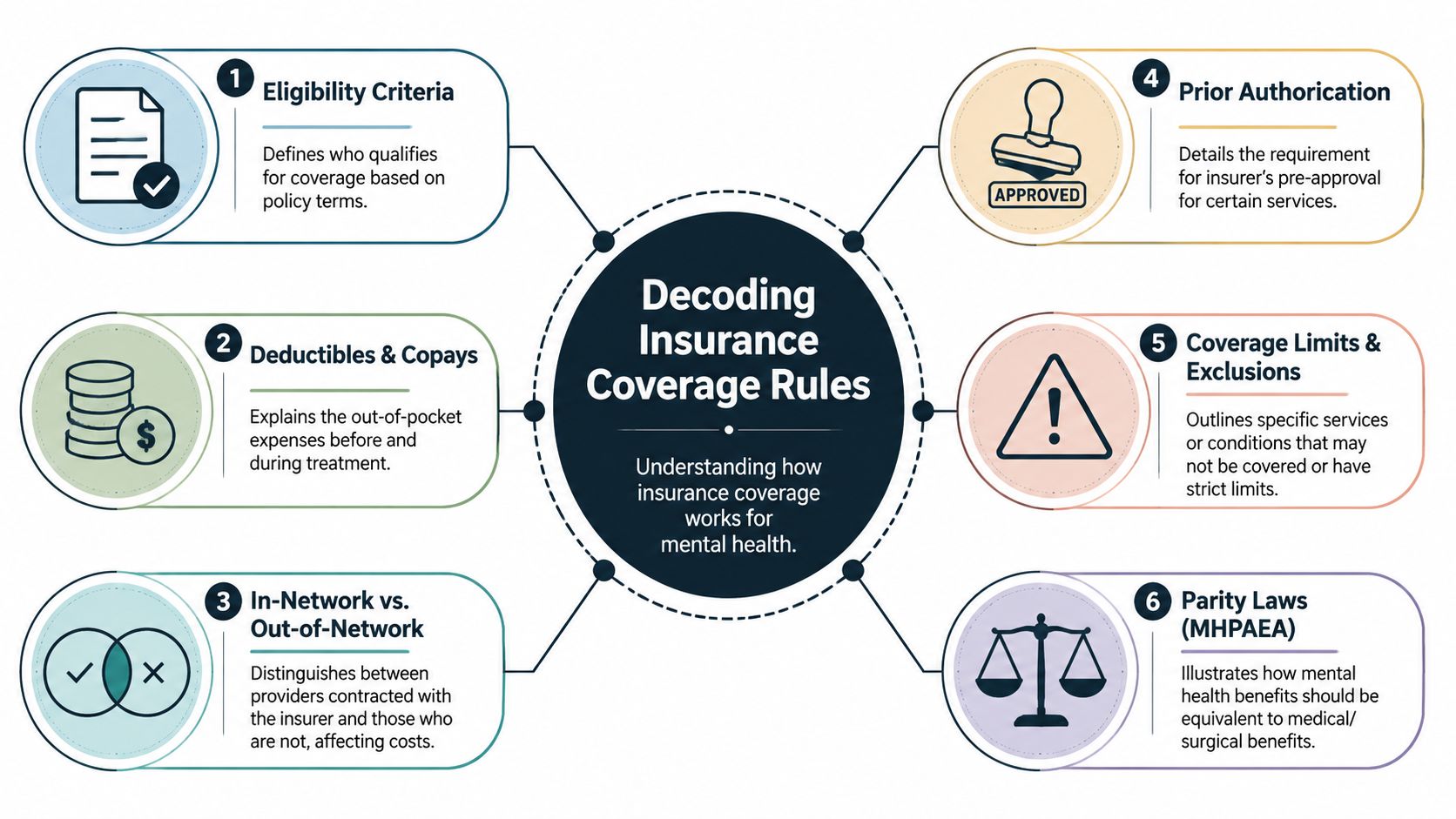

Understanding the Rules of Insurance Coverage

A patient calls after finally deciding to get help. The first question sounds simple. “Is therapy covered?” The full answer usually depends on a small set of insurance rules that decide what gets approved, what gets reviewed, and what the patient may still owe.

Medical necessity comes first

Insurers usually start with medical necessity. They want clinical documentation showing that treatment addresses a diagnosed mental health or substance use condition, not general stress relief or personal growth alone.

That review often includes three basic questions. Is there a recognized diagnosis? Does the recommended service match that diagnosis? Is the level of care reasonable based on symptoms, safety concerns, and treatment history?

This is often the point where patients go from confused to clear. A policy may include behavioral health benefits, but coverage still depends on how the need for care is documented.

Network status changes what you pay

The next rule is network status. In-network providers have contracted rates with the insurer. Out-of-network benefits may still exist, especially with PPO plans, but patients often face higher costs, separate deductibles, balance billing exposure, or claim forms they must submit themselves.

That trade-off matters. A provider may be clinically appropriate and available quickly, but the insurance cost can be higher if the provider is outside the plan's network. Patients comparing programs should ask both questions at the same time: “Is this clinically the right fit?” and “How will my plan process these claims?”

For readers comparing higher-end treatment options, this guide on whether insurance can cover luxury rehab explains how plan rules apply when the setting itself raises cost questions.

Prior authorization affects timing

Some services need prior authorization before treatment begins or shortly after admission. This is more common for intensive outpatient programs, partial hospitalization, residential treatment, and detox than for standard weekly therapy sessions.

Prior authorization does not automatically mean the insurer is resisting care. It usually means the plan wants records, an assessment, or physician documentation before approving that level of treatment. Delays happen when patients ask only whether therapy is covered and do not ask what approval steps apply to the specific program.

I often tell families to listen for exact language. “Covered” is not the same as “authorized,” and “authorized” is not the same as “paid in full.”

The policy terms that change the final bill

Patients do not need to memorize insurance law, but they do need to understand the terms that shape out-of-pocket cost.

| Term | What it means in practice |

|---|---|

| Deductible | The amount the member may have to pay before certain benefits start paying |

| Copay | A fixed amount due for a covered visit or service |

| Coinsurance | The percentage of the allowed amount the member pays after deductible rules are met |

| Visit limit | A session cap in some plans, though other plans manage use through authorization instead |

| Out-of-pocket responsibility | The member's share after the plan applies its payment rules |

Plans also cannot apply tougher behavioral health rules than they apply to comparable medical or surgical benefits. In plain language, mental health care cannot be singled out for stricter financial or treatment limits because it is behavioral health.

Why comparison helps

Patients often understand these rules better when they see that insurers use the same framework across many specialized services. Diagnosis, medical necessity, coding, exclusions, and prior approval come up in other categories too. This overview of insuring hyperbaric oxygen therapy shows how similar coverage logic appears outside behavioral health.

At the admissions stage, the goal is clarity. Patients need to know what service is being requested, what the plan requires, what the likely cost-sharing will be, and who is handling the verification work. That is how insurance stops feeling like a wall and starts becoming a checklist.

Examples of Covered vs Uncovered Services

A patient calls after seeing two programs online that both say they offer therapy. One is likely billable through insurance. The other may be entirely self-pay. The difference usually comes down to whether the service is medical treatment, how it is documented, and whether the plan recognizes that level of care.

Insurers usually do not decide coverage based on comforting language such as healing, growth, or recovery. They look for a diagnosed condition, a covered service, and records showing why that service is medically necessary. In practice, that means a therapy session tied to a mental health or substance use diagnosis is often treated very differently from coaching, retreat programming, or general wellness support.

Common examples that are usually covered

These services often fit standard behavioral health benefits when the clinical record supports them:

- Individual psychotherapy for a diagnosed condition: Therapy for depression, anxiety, trauma-related symptoms, or substance use disorder that follows a treatment plan.

- Psychiatric evaluation and medication management: Assessment of symptoms, diagnosis, and follow-up care related to a recognized mental health condition.

- Group therapy within addiction treatment: Group sessions that are part of a structured treatment program for a documented substance use disorder.

- Family therapy tied to the patient’s treatment: Sessions focused on relapse prevention, communication around symptoms, or discharge planning for the identified patient.

- Higher levels of care: Intensive outpatient, partial hospitalization, detox, and residential treatment may be covered when the clinical picture shows outpatient therapy alone is not enough.

Common examples that are often not covered

These services are valuable to some patients, but they are often outside standard medical reimbursement:

- Life coaching: Support with goals, habits, or motivation without a billable medical service.

- Relationship counseling without a qualifying diagnosis: Couples work focused only on communication or enrichment.

- Wellness retreats: Restorative programming, spa services, or lifestyle experiences that are not documented as medical treatment.

- Personal growth counseling: Self-exploration or development work without a diagnosed disorder or covered therapy service.

A simple test helps. Ask, “Is the plan paying for treatment of a documented condition, or for a general benefit to well-being?” Insurance usually pays for the first category.

A side-by-side view

| Usually covered | Often not covered |

|---|---|

| Therapy tied to a diagnosed mental health condition | Counseling for general self-development |

| Substance use treatment for a documented disorder | Wellness programming without medical necessity |

| Family sessions supporting a patient’s recovery plan | Relationship support with no qualifying diagnosis |

| Structured outpatient or day treatment when clinically indicated | Elective services outside recognized behavioral health treatment |

This distinction matters even more in specialty addiction care, where program websites can look similar while insurance treatment rules are not. Patients comparing higher-end options often benefit from a clearer explanation of whether insurance can cover luxury rehab, especially when the core question is which clinical services inside the program are billable and which amenities are not.

In admissions, this is often the moment when confusion starts to lift. Once the patient knows what part of care is clinical, what part is non-covered, and what the insurer needs to approve payment, the decision becomes much easier.

Your Step-by-Step Insurance Verification Checklist

A short call to the insurer can prevent a costly misunderstanding later. The key is to ask narrow questions, write down the answers, and confirm the details that affect actual payment.

Step 1

Find the right number on the insurance card. The best line is usually the one for behavioral health, mental health, substance use treatment, or member services. If the card only shows a general number, the representative can transfer the call.

Before calling, gather the policy number, group number, full legal name of the member, and the date of birth. If a facility is helping with verification, have the facility name and level of care ready.

Step 2

Ask about the exact type of care being considered. Vague questions produce vague answers.

A stronger approach is to ask questions like these:

- Outpatient therapy: Is individual psychotherapy covered under the plan, and what are the in-network and out-of-network benefits?

- Addiction treatment: Does the plan cover substance use disorder treatment at outpatient, intensive outpatient, partial hospitalization, detox, or residential levels?

- Authorization: Is prior authorization required for any of these levels of care?

- Network rules: Does the plan include out-of-network benefits for behavioral health?

- Claims process: If the provider is out of network, does the member submit claims, or can the provider submit on the member’s behalf?

Step 3

Ask what the member will owe. “Covered” doesn't mean “free.”

Use this checklist during the call:

- Deductible status: Has the deductible been met?

- Copay or coinsurance: What applies to this service?

- Session or stay limits: Is there a cap on visits or days?

- Medical necessity review: Who decides that the requested level of care is appropriate?

- Exclusions: Is anything specifically excluded from this benefit?

Step 4

Document the conversation. Write down the representative’s name, the date, the time, and any call reference number. That record helps if a later claim is processed differently than what was explained on the phone.

A simple note in a phone app is enough, as long as it includes the essentials. Patients often skip this step and then have nothing concrete to refer to when billing questions appear later.

Step 5

If treatment is being considered at a facility, let the admissions team verify benefits independently. Facilities often know which wording to use, what level of care to request, and which details need clarification before admission. For a plan-specific example, this guide to using Aetna benefits for rehab in California shows the kind of questions that matter during verification.

Step 6

If a claim is denied, ask for the denial reason in writing and review the appeal process. Denials may relate to missing records, coding issues, network confusion, or disagreement about level of care. An appeal is usually stronger when it includes clinical documentation and a direct response to the denial reason.

A denial isn't always the final answer. Sometimes it's the start of a better-documented review.

How Oceans Luxury Rehab Simplifies Your Path to Recovery

A lot of patients reach this stage exhausted. They have already decided they need help, but now they are staring at insurance cards, intake forms, unfamiliar treatment terms, and the risk of choosing the wrong level of care or the wrong facility for their plan.

That confusion is common in addiction and mental health treatment because coverage questions rarely stop at one service. A patient may need detox first, then residential care, then a step down to PHP, IOP, or outpatient support. Each level can trigger different rules, reviews, and out-of-pocket costs.

Why direct admissions support matters

Having insurance does not automatically make treatment simple to access. Patients still have to confirm whether the facility is in network, whether out-of-network benefits apply, whether preauthorization is required, and how the insurer defines medical necessity for the requested level of care.

That is where a skilled admissions team saves time and prevents expensive misunderstandings.

For a patient, the goal is clarity. For an admissions team, the job is to turn scattered insurance information into a workable plan. That means reviewing the policy, identifying the likely level of care, checking for approval requirements, and explaining what may still be the patient's responsibility before admission.

Patients who want an outside reference can review these steps for checking network status. It offers a practical framework for confirming provider status and knowing which questions to ask before treatment begins.

What good admissions work looks like

A strong admissions process should do more than collect policy details. It should help a patient move from uncertainty to a clear next step.

That usually includes:

- Benefit review: checking behavioral health coverage, deductibles, coinsurance, out-of-pocket limits, and any out-of-network provisions

- Level-of-care review: matching the patient's clinical needs to detox, residential, PHP, IOP, or outpatient treatment

- Authorization coordination: gathering the clinical and insurance information needed for utilization review

- Cost discussion: explaining what insurance may pay for and where patient responsibility may remain

- Privacy protection: handling personal and family information carefully during intake

This work matters because the trade-offs are real. A lower level of care may sound more affordable at first, but it may not be clinically appropriate. A higher level of care may fit the clinical picture, but it can require more insurer review. Patients need both answers at the same time: what is medically appropriate, and what is financially realistic.

How Oceans Luxury Rehab helps reduce friction

Oceans Luxury Rehab helps patients handle that process with admissions support tied to the actual services being considered. The program is located in San Clemente in Orange County and offers medically supervised detox, residential inpatient treatment, partial hospitalization, intensive outpatient care, outpatient services, dual-diagnosis support, and evidence-based therapy in a private oceanfront setting.

For patients and families, that structure can simplify decisions. Instead of calling multiple providers and trying to compare incomplete insurance answers, they can work with one team that understands the continuum of care and how insurers typically review each stage.

That does not mean every question is answered instantly or every service is automatically approved. It means the patient has experienced staff helping verify benefits, explain likely approval issues, and prepare for the next step before admission starts.

From confusion to a plan

The difference between raw insurance information and useful guidance is significant, especially when someone is dealing with substance use, depression, anxiety, trauma, or a family crisis.

Patients do better when they know what their plan may cover, what still needs confirmation, and what the admissions path looks like from the first call onward. That clarity lowers stress and helps them focus on treatment instead of policy language.

If insurance questions are delaying care, Oceans Luxury Rehab can help verify eligible PPO benefits, explain the likely approval path, and discuss appropriate levels of care in a private California setting.