A family often reaches this question at the worst possible moment. Someone has finally said yes to treatment, emotions are already running high, and then the next problem appears fast: does insurance cover inpatient rehab, and if so, how much?

That confusion stops many people in their tracks. One person is searching the insurance portal. Another is staring at an ID card. Someone else is trying to figure out the difference between a deductible and a copay while also worrying about detox, work leave, privacy, and what happens if treatment is delayed.

The good news is that inpatient rehab is not outside the insurance system. In many cases, coverage exists. The challenge is understanding what the policy pays for, what the insurance company considers medically necessary, and what part of the stay may still become the patient’s responsibility.

This guide breaks that process down in plain language. It explains why addiction treatment is generally covered, how common insurance terms affect the bill, why PPO plans matter so much for luxury rehab in California, and what families should do when they need quick answers without spending hours on hold.

Navigating the Path to Recovery and Paying for It

A common scene plays out the same way in many homes across California. A spouse finds hidden bottles again. A parent gets a call from work about missed shifts. An adult child admits that pills, alcohol, or another substance have taken over daily life. Everyone agrees that inpatient treatment is needed. Then the practical question lands with full weight: how is this going to be paid for?

That question can feel cold when the primary issue is survival, safety, and getting someone stabilized. Still, it matters. Families need to know whether the insurance plan helps with detox, residential care, physician visits, therapy, and the length of stay. They also want to know whether a private room, added privacy, and a calmer environment change what insurance will pay.

What makes this harder is that insurance language rarely sounds human. Policies talk about benefits, exclusions, coinsurance, prior authorization, and out-of-network reimbursement. Families are left translating legal and billing language at the same time they’re trying to help someone enter treatment.

A clear insurance answer can lower panic quickly. Once a family understands what the plan covers, decisions become much easier.

The most useful shift is moving from a yes-or-no mindset to a coverage-details mindset. For many people, the answer to “does insurance cover inpatient rehab” is yes, at least in part. The main work is confirming:

- What level of care is covered: Detox, residential treatment, physician services, and mental health support may be handled differently under one plan.

- Which facility status matters: In-network and out-of-network rules can change the bill in a major way.

- What costs remain: Even with coverage, the patient may still owe a deductible, copay, coinsurance, or charges tied to upgrades.

Families don't need to master all of that before making the first call. They only need to know that insurance coverage for inpatient rehab is often possible, and that the details can be verified before admission decisions are finalized.

Why Your Insurance Plan Must Cover Addiction Treatment

A family may feel like they are asking for special permission when they call about rehab. In reality, they are asking how a health plan applies a covered benefit to a serious medical condition.

Addiction treatment is part of modern health coverage

Under the Affordable Care Act, individual and small group plans generally must include mental health and substance use disorder treatment as covered health benefits. Federal parity rules also require insurers to treat behavioral health benefits in a manner comparable to medical and surgical benefits, as explained by the Centers for Medicare & Medicaid Services overview of mental health and substance use disorder parity protections.

For families, that changes the question from "Will insurance help at all?" to "What does this specific plan cover, and what rules apply?"

Plainly stated, addiction care is not supposed to sit outside real medicine. Detox, residential treatment, physician oversight, therapy, and psychiatric support are part of healthcare.

What parity actually means

Parity is a legal word, but the practical idea is simple. An insurer cannot place tougher financial or treatment barriers on addiction care just because it falls under mental health or substance use treatment.

A helpful comparison is a broken bone versus alcohol dependence. A plan cannot freely cover one because it looks more familiar, then build extra hurdles around the other because it is behavioral health.

That does not guarantee automatic approval for every admission or every length of stay. It does mean the insurer must use standards that are comparable.

For families, that often shows up in a few important ways:

- Addiction history alone should not block coverage. A plan cannot treat substance use treatment as less legitimate care.

- Behavioral health benefits cannot be singled out for worse limits by default. Coverage rules must be comparable to medical benefits.

- Medical necessity reviews still happen. The review process has to follow fair plan standards, not stigma.

Practical rule: You are not asking for a favor. You are asking the insurer to apply the behavioral health benefit your plan already includes.

Why the answer still feels complicated

Coverage law creates the floor. Your individual policy decides how payment works in real life.

That is why two people can both have PPO insurance and still get very different cost estimates. One plan may reimburse a larger share of residential care. Another may require preauthorization. A third may cover the clinical side of treatment while leaving non-clinical comfort features outside the reimbursable amount.

This point matters for clients considering luxury inpatient rehab in California. PPO plans often offer more flexibility than restrictive plan types, which can be especially helpful when a family wants privacy, a quieter setting, strong clinical support, and a higher level of comfort. At the same time, insurance usually pays based on covered treatment services, not on every premium feature attached to the stay. That distinction helps families ask better questions early, especially if they are exploring insurance coverage for drug rehab and residential treatment options.

A simple way to view it is this. The law says addiction treatment belongs in health coverage. The plan then applies network rules, authorization rules, and reimbursement formulas to a specific facility and level of care.

The key takeaway

For many families, the grounded answer to "does insurance cover inpatient rehab" is yes, at least in part. The more useful question is how a PPO plan applies those benefits to a private, high-comfort inpatient setting in California, and which portion of the stay will be covered versus paid out of pocket.

Decoding Your Insurance Policy Key Terms and Costs

Insurance documents often confuse people because they describe payment in layers. A simpler way to read them is to think of treatment like a bill with several parts. One part is what must be paid first, one part is shared, and one part is the limit on what the patient may have to pay during the plan year.

The terms that affect the real bill

The words below show up again and again during rehab admissions. Once they make sense, conversations with an insurer become far less intimidating.

| Term | What It Is | How It Works |

|---|---|---|

| Deductible | The amount the patient must pay before the plan starts sharing more of the cost | If the deductible hasn't been met, early treatment charges may apply to the patient first |

| Copay | A fixed amount tied to a service or visit | Some plans use copays for certain services, though inpatient treatment often involves broader cost-sharing rules |

| Coinsurance | A percentage share of the cost after the deductible or after coverage rules apply | The insurer pays part and the patient pays part until the plan's limits are reached |

| Out-of-pocket maximum | The yearly cap on certain covered patient costs | After that point, the plan may pay covered costs at a higher level for the rest of the plan year |

| In-network | A provider with a contract and negotiated rates with the insurer | This usually lowers the patient’s responsibility |

| Out-of-network | A provider without that same contract structure | The plan may reimburse differently, cover less, or require more from the patient |

A family doesn't need to memorize these terms. They need to know which of them changes the amount due at admission and during the stay.

A simple example without the legal jargon

Suppose a person needs detox and residential treatment. The insurer may first check whether the level of care is medically necessary. If it is, the plan then applies its payment rules.

One policy may say the deductible must be met first. Another may begin sharing covered costs sooner. A PPO may allow more flexibility in facility choice, while another plan may tie most benefits to a tighter network.

That’s why two people with “good insurance” can get very different answers about the same kind of treatment.

Some of the most stressful billing surprises don't come from lack of coverage. They come from misunderstanding network status and cost-sharing before admission.

PPO versus HMO in real life

A lot of confusion around does insurance cover inpatient rehab comes down to plan type.

PPO plans

A PPO, or Preferred Provider Organization, usually gives the member more flexibility. That can matter a lot in addiction treatment, especially when a family is looking for privacy, dual-diagnosis support, or a specific California location.

PPOs often allow access to a wider range of providers and may still offer some level of coverage outside the preferred network. The exact benefit still depends on the plan.

HMO plans

An HMO, or Health Maintenance Organization, usually works through a more controlled network structure. Referrals and network restrictions often matter more. If the desired treatment center falls outside that structure, access may become more complicated.

For families trying to move quickly, those restrictions can delay decisions.

The questions that actually matter

Many people ask the insurer broad questions and get broad answers back. Better results come from asking narrower questions tied to admission.

- Is inpatient substance use treatment covered under this plan?

- Does the plan require prior authorization for residential treatment?

- What is the deductible status right now?

- What cost-sharing applies after admission?

- Is the facility considered in-network or out-of-network?

- Are physician services billed separately from the residential stay?

Families who want a deeper overview of plan basics can review this related guide on whether insurance covers drug rehab.

One benchmark that helps people understand cost-sharing

Medicare provides a useful example of how structured rehab coverage can work, even though private insurance often works differently. For inpatient rehabilitation care in 2026, after the Part A deductible of $1,736, beneficiaries pay $0 for days 1 through 60 in an inpatient rehabilitation facility. For days 61 through 90, the daily coinsurance is $434. For lifetime reserve days beyond that, the daily coinsurance rises to $868, after which all costs fall to the patient. Medicare also reported that it spent $8.7 billion on IRF care in 2019 for 363,000 fee-for-service beneficiaries, supporting 409,000 stays across 1,150 facilities, and accounted for 58% of IRF discharges with a 67% average occupancy rate, according to Medicare’s inpatient rehabilitation coverage overview.

That example doesn't define what a private PPO will do for addiction treatment. It does show that rehab coverage is a real, structured insurance benefit, not a fringe exception.

Using Your PPO Plan for Luxury Rehab in California

When a person has a PPO plan, the question usually changes from “Is there any coverage?” to “What exactly counts as covered care inside a luxury setting?”

That distinction matters. High-comfort treatment environments often include features that families value greatly, especially when privacy, executive concerns, trauma history, or co-occurring mental health conditions are involved. But insurers separate medical necessity from amenity preference, and that’s where confusion starts.

What PPO plans usually do well

A PPO often offers the flexibility that luxury rehab clients need most. It may provide broader provider choice and a less restrictive path to accessing specialized addiction treatment than tighter network plans.

For inpatient rehab, the insurer may cover core clinical elements such as detox support, therapy, psychiatric care, medication management, and coordinated treatment planning when those services are medically necessary. In a luxury setting, the policy may still cover the treatment itself even if it doesn't cover every upgrade attached to the setting.

That’s why private rooms, upgraded accommodations, or added wellness features can become the dividing line between covered treatment and personal financial responsibility.

Covered treatment versus uncovered upgrades

A useful way to think about a luxury program is to separate the clinical package from the comfort package.

What may be treated as covered care

If a person needs structured inpatient treatment for substance use and co-occurring mental health symptoms, the insurer may evaluate clinical needs such as:

- Detox and stabilization

- Psychiatric assessment

- Medication management

- Individual and group therapy

- Dual-diagnosis treatment

- Physician oversight tied to medical necessity

What may be treated as an upgrade

Some plan designs exclude or limit charges tied only to comfort or preference, such as:

- Private accommodations requested for convenience alone

- Premium meals or hospitality-style extras

- Non-medical amenities not bundled into the covered treatment model

That doesn't mean a luxury setting is automatically excluded. It means the facility and insurer need to align on what part of the stay is clinically necessary and what part falls outside standard coverage.

Privacy can be clinically relevant. But it usually needs to be documented as part of treatment necessity, not described only as a preference.

Why documentation changes outcomes

California PPO clients often experience the most significant distinction. PPO coverage can be strong, but authorization decisions still depend on clinical presentation and documentation.

According to this insurance coverage discussion for rehab treatment, PPO plans often cover inpatient rehab but may exclude non-medically necessary luxuries. That same source notes that facilities can negotiate approvals by certifying the need for intensive coordinated care for clients with dual-diagnosis needs, though patients may still face out-of-pocket costs for upgrades. It also notes rising denials tied to luxury settings in California, which is why careful insurance navigation matters.

In practical terms, a patient with addiction plus anxiety, depression, trauma symptoms, or relapse risk may have a stronger clinical case for a highly structured and private setting than someone seeking only upgraded surroundings.

Why PPO flexibility matters in California

California families often want more than basic containment. They may need confidentiality, distance from local triggers, strong mental health support, and an environment where a person can rest enough to stay engaged in treatment.

That’s one reason PPO plans are often the most workable insurance route for high-comfort residential care. A PPO can offer room to pursue a treatment setting that matches the person’s clinical and personal needs, even if the final coverage still depends on verification and authorization.

For readers comparing options, this related page on using PPO insurance for luxury addiction treatment in California explains that model in more detail.

One caution families should keep in mind

Luxury rehab and medically necessary rehab are not always billed the same way. A family may hear that treatment is covered and assume every part of the stay is covered. That assumption creates surprise bills.

A better approach is to confirm these issues before admission:

- Whether the plan covers the inpatient level of care

- How the insurer classifies the facility and services

- Whether any room type or amenity charge is carved out

- What the estimated patient responsibility may be

The strongest PPO outcome usually comes from aligning clinical need, documentation, and benefit verification before the admission date.

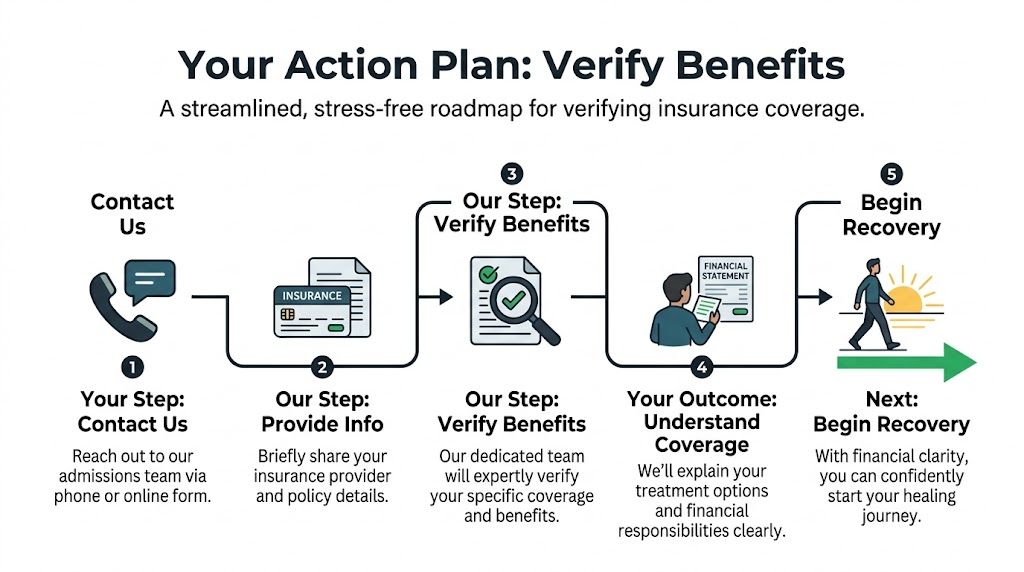

Your Action Plan How to Verify Benefits in One Simple Step

A family may reach the point of seeking help on a Sunday night, with one person asking, “Can we admit tomorrow?” and another asking, “Will insurance pay for this?” In that moment, verification feels larger and more complicated than it is.

For most PPO admissions, the next step is simple. Give the admissions team your insurance information and a short clinical snapshot, then let them check the policy and explain the results in plain language. It works like handing a pharmacist your prescription card. You are not expected to decode the policy on your own before help can begin.

What the family actually needs to provide

Many families assume they need a full medical packet before anyone can answer basic coverage questions. In practice, the first stage usually requires only the insurance card, the policyholder’s details, and a brief summary of the current situation.

That summary may include the primary substance involved, whether withdrawal or detox concerns are present, how recent the use has been, and whether anxiety, depression, trauma, or other mental health symptoms are part of the picture. The goal is not perfection. The goal is to give the verifier enough context to ask the insurer the right questions about inpatient care, especially when the family is looking at a private, high-comfort setting in California.

What happens behind the scenes

A good verification review goes far beyond asking whether “rehab” is covered. That word is too broad to help a family make a decision. An experienced admissions team breaks the policy into parts that affect real life: level of care, network status, expected out-of-pocket cost, and any limits tied to upgraded accommodations or privacy features.

For clients considering Oceans Luxury Rehab, that matters because PPO plans may cover the treatment itself while handling certain room or amenity charges differently. Families who value discretion, comfort, and a calmer environment need that distinction explained before admission, not after.

Benefit confirmation

The insurer is usually asked whether the plan includes benefits for detox, residential treatment, physician services, medication management, and mental health care connected to substance use treatment.

Network review

The verifier checks how the facility is processed under the member’s specific PPO plan and what that means for reimbursement, coinsurance, and any out-of-network exposure.

Cost estimate

The team reviews how much of the deductible has been met, whether a copay or coinsurance applies, and which charges may remain the patient’s responsibility.

Authorization requirements

If the insurer requires prior authorization or a clinical review, the team can identify that early and prepare the next steps before the admission date is on the line.

Families usually need answers to three practical questions. Is inpatient treatment covered, what will likely cost extra, and what has to happen before admission?

Why this matters so much in addiction treatment

Readiness for treatment can be brief. A person who says yes today may feel very different 48 hours from now. Verification helps protect that window by replacing guesswork with a clear plan.

It also reduces a common source of confusion with luxury rehab. Insurance may cover medically necessary services, but not every comfort feature is billed the same way. Clear verification helps a family separate covered clinical care from optional upgrades, so they can make a decision with open eyes.

Oceans Luxury Rehab offers benefit verification for families exploring treatment and explains expected patient responsibility before admission decisions are finalized.

The best way to ask for verification

A strong request can be short. The admissions team usually needs four categories of information:

- Insurance details: Member ID, group number, insurer name, and the policyholder’s full name

- Treatment need: Alcohol, opioids, stimulants, prescription medication misuse, or multiple substances

- Current urgency: Detox symptoms, recent relapse, safety concerns, or mental health instability

- Timing: Whether the family is hoping for immediate admission or planning for the next few days

Families with plan-specific questions can also review this guide to using Aetna benefits for rehab at Oceans Luxury Rehab in California.

What families should expect back

A useful verification response should sound clear, not technical. It should answer the questions a family can act on:

| What Families Need to Know | Why It Matters |

|---|---|

| Whether inpatient rehab is covered | This shows whether the plan recognizes the residential level of care being requested |

| Whether authorization is required | This helps prevent delays before admission |

| What the likely patient portion is | This helps the family prepare financially |

| Whether any private-room or luxury component may be excluded | This clarifies the gap between covered treatment services and elective upgrades |

If anything still feels uncertain, ask one direct follow-up question: “What is confirmed now, and what depends on clinical review?” That often turns a confusing insurance conversation into a clear next step.

Overcoming Hurdles Preauthorization and Potential Denials

A family may feel ready to admit their loved one today, then hear one discouraging sentence from the insurer: “We need prior authorization.” In that moment, it can sound like the door just closed. Usually, it means the insurer wants proof that residential treatment is the right level of care before payment is approved.

That distinction matters.

Preauthorization is the insurer’s review process. It is not the same as a final refusal. For families considering a private, high-comfort program in California, including Oceans Luxury Rehab, this step often becomes the point where clinical need and plan rules have to line up clearly. The treatment setting may offer privacy, upgraded accommodations, and a calmer environment, but the insurance company is still asking a narrower question. Does the clinical record support inpatient rehab?

What preauthorization usually involves

Insurers commonly ask for a picture of the person’s current condition, not just their diagnosis. That can include recent substance use, withdrawal symptoms, relapse pattern, overdose history, medical concerns, psychiatric symptoms, sleep disruption, impaired functioning, and any immediate safety risk.

A useful way to understand this is to picture a boarding pass at the gate. Having a ticket does not always get someone onto the plane by itself. The airline still checks that the name, time, and destination match. Preauthorization works in a similar way. The plan may include behavioral health benefits, but the insurer still checks whether the request matches the level of care being sought.

For luxury inpatient rehab, one point often causes confusion. Insurance may cover the treatment itself while excluding some nonclinical comfort features. Families should separate those two questions early:

- Is residential addiction treatment medically approved?

- Are any private-room, premium-amenity, or elective comfort costs outside the covered benefit?

That separation can make a stressful conversation much easier to follow.

Why denials happen

Many denials begin with a mismatch between what was requested and what was documented. The insurer may say the records do not show enough withdrawal risk, enough failed lower levels of care, or enough instability to justify inpatient treatment. In other cases, the problem is administrative. Missing notes, delayed records, an out-of-network issue, or an incomplete clinical review can all slow approval.

A denial also does not always mean the insurer thinks treatment is unnecessary. It may mean the insurer wants detox reviewed first, outpatient treatment considered first, or more detail from the clinical team. Families often hear “no” when the actual message is “not yet documented clearly enough.”

A denial often points to a gap in records or level-of-care support. It does not always end the admission process.

Where public insurance fits, and where it often doesn't

Families in California often ask about Medi-Cal as a backup option. Medi-Cal does cover many substance use services, but access to private residential programs with a high level of privacy and comfort is often more limited than with a PPO plan.

That matters for people seeking treatment in a discreet, premium setting. A PPO plan usually offers more flexibility for private providers and out-of-network reimbursement. For someone trying to enter a quiet, oceanfront residential program rather than a standard facility, that difference can shape what options are realistically available.

What to do if coverage gets complicated

Start by slowing the conversation down. Insurance calls move fast, and families are often taking notes while scared and sleep-deprived. Ask the representative or admissions team to explain the issue in plain language.

Then work through these questions one by one:

- What is the exact reason for the delay or denial? Ask whether the issue is medical necessity, missing records, network status, or plan exclusions.

- Can that reason be sent in writing? Written explanations are easier to review and challenge.

- Is a peer-to-peer review available? That allows the treating clinician to speak directly with the insurer’s reviewer.

- Does the insurer need more clinical detail? If so, ask what specific symptoms, risks, or history are still unclear.

- Is the problem the treatment level or the luxury component? Covered clinical care and noncovered upgrades are not always treated the same way.

Families should not feel embarrassed asking these questions twice. Insurance language can be confusing even for professionals.

The practical goal is simple. Get the insurer to say, as clearly as possible, whether the barrier is paperwork, medical review, network rules, or a noncovered amenity. Once that is clear, the next step becomes easier to choose.

Begin Your Recovery at California's Premier Treatment Center

Once the insurance questions are handled, the focus can return to where it belongs. Recovery. Safety. Sleep. Stabilization. A chance for the person and the family to breathe again.

Inpatient treatment should provide more than a bed and a schedule. It should create enough calm for a person to stop spiraling, step out of the chaos of active addiction, and begin doing the hard clinical work with dignity. For many adults in Southern California, especially professionals and people carrying major personal pressure, privacy is not a luxury in the casual sense. It helps create the conditions for honesty and engagement.

At a high-comfort oceanfront setting in San Clemente, that can mean quieter surroundings, private accommodations, physician oversight, nursing support, individualized treatment planning, and integrated care for both substance use and mental health symptoms. Those details matter because recovery isn't just about getting substances out of the body. It's about helping the person stay long enough, feel safe enough, and stabilize enough to absorb treatment.

Families often reach this point exhausted. They've spent weeks or years trying to manage fear, secrecy, broken promises, and medical risk. They don't need more confusion. They need a direct path into care and a setting that supports real healing.

That’s why the insurance question matters so much. Not because billing is the main story, but because financial clarity removes one more barrier between a struggling person and treatment. Once that barrier is lowered, admission becomes possible, and possibility is often what families have been missing.

The answer to does insurance cover inpatient rehab is often yes, at least in part. The next step is confirming how the plan applies to the specific treatment setting, level of care, and clinical need. With those answers in hand, the path forward becomes much more manageable.

When a family is ready to verify benefits and discuss treatment options confidentially, Oceans Luxury Rehab can be the next step. The admissions team can review insurance details, explain likely coverage for inpatient rehab, and help families move toward care in a calm, clear, and supportive way.