A family can be ready to get help for a son, daughter, spouse, or parent, then hit a sudden wall when the insurance card says UMR and no one is sure what those letters mean. In a rehab crisis, that kind of confusion can slow down the call, delay an assessment, and add stress to an already painful night.

UMR stands for United Medical Resources. It is a third-party administrator, which means it often handles claims, eligibility, and plan support for an employer health plan rather than acting as the insurer that funds care.

For a family in crisis, that distinction is important because UMR usually is not the obstacle. It is often the organization helping process the benefits tied to the plan.

If you are looking for addiction treatment, the practical question is not just, “What does UMR stand for?” The more urgent question is, “What does this plan cover for detox, residential rehab, therapy, and other substance use treatment?” Once you separate the name on the card from the way the plan works, the path gets clearer, and it becomes much easier to take the next step toward care at a luxury rehab facility in California.

Decoding Your Insurance Card When You See UMR

Seeing UMR on an ID card or explanation of benefits often raises the same question. What does UMR insurance stand for, and is it the same as the actual insurance company?

The plain answer is United Medical Resources. UMR is known as the nation's largest third-party administrator, specializing in administering self-funded health plans for employers and organizations, as explained by InsuranceProviders on what UMR stands for.

Why this confuses so many families

An insurance card is typically expected to show the name of the company paying for care. With UMR, that isn't always how it works. The employer may fund the plan, another large healthcare brand may provide the network, and UMR may handle the day-to-day administration.

That means a person can hold a card with UMR on it and still have coverage that depends on the employer's plan design. The letters on the card identify the administrator handling claims and support. They don't automatically tell a family every detail about detox, residential rehab, counseling, or medication coverage.

Practical rule: If UMR appears on the card, the next step isn't to panic. It's to verify the exact behavioral health and substance use benefits tied to that employer plan.

What families should look for first

When UMR appears on plan paperwork, these are usually the most useful places to start:

- Member ID details: The member ID helps the admissions or billing team locate the exact plan.

- Customer service phone number: The number on the back of the card often connects the family to benefit verification support.

- Network references: Some cards or documents mention the provider network used by the plan.

- Plan-specific language: Terms like self-funded, PPO, or behavioral health benefits can shape what rehab services are covered.

For a family in crisis, this distinction matters because UMR isn't the roadblock. It's often the gateway to figuring out what treatment can be approved and how quickly admission can move forward.

What Is a Third-Party Administrator Like UMR

A third-party administrator, often shortened to TPA, runs the day-to-day parts of a health plan. With UMR, that usually means handling the member-facing and administrative work for an employer-sponsored plan instead of acting as the company that insures the risk itself.

Families often run into this term during a stressful moment. A son needs detox. A spouse needs residential rehab. The insurance card says UMR, but the answers about coverage still feel unclear. That confusion happens because UMR's job is administrative. It helps operate the plan, but the employer's plan documents still shape what treatment is covered and what approval steps may apply.

The role is similar to property management. The owner pays for the building and sets the rules. The management company handles leases, maintenance requests, and day-to-day communication. In the same way, an employer may fund the health plan while UMR handles claims, eligibility checks, and member support.

What UMR usually handles

UMR's administrative responsibilities often include:

- Claims processing: Reviewing and processing medical and behavioral health claims.

- Customer support: Answering questions about benefits, eligibility, and plan procedures.

- Provider coordination: Connecting members to the provider network tied to the plan.

- Eligibility verification: Confirming whether coverage is active and which services may fall under the plan.

That distinction matters more than it may seem at first.

For addiction treatment, the family usually needs answers to practical questions right away. Is detox covered? Does residential treatment require prior authorization? Is the facility in network? A TPA like UMR may help process those steps, but the final benefit structure still depends on the employer's plan design, including deductibles, copays, coinsurance, and out-of-pocket limits.

This is one reason two people with UMR on their cards can have very different rehab benefits. One plan may include strong behavioral health coverage. Another may have tighter rules around authorization or length of stay. If your family is also trying to sort out therapy benefits, this guide to UnitedHealthcare counseling coverage can help clarify how behavioral health administration and network access often fit together.

A helpful way to frame it is this: UMR is often the operator of the plan's daily mechanics, while the employer remains the one that selected the plan structure. That setup is common among employer health plans and aligns with the broader market categories discussed in PIA Southern Alliance's top carriers.

For a family seeking treatment at a luxury rehab in California, this means the fastest path is not guessing from the card alone. It is confirming the exact rehab benefits tied to that specific plan, then matching those benefits to the level of care your loved one needs now.

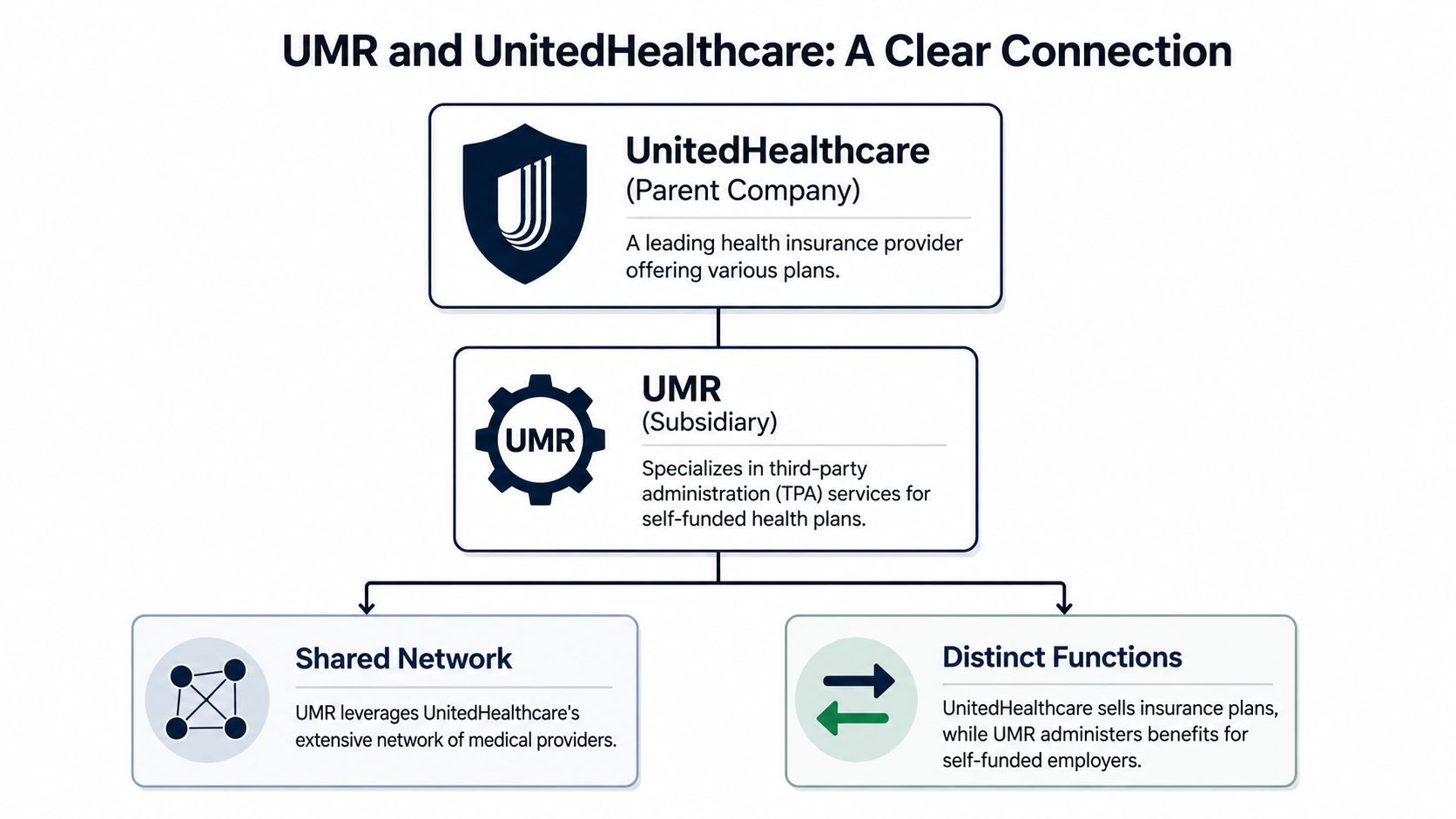

The Relationship Between UMR and UnitedHealthcare

A family can be on the phone with admissions, look at the insurance card, and hear two names in the same conversation: UMR and UnitedHealthcare. That often sounds like two separate insurance plans. In practice, it is usually one plan with different parts doing different jobs.

UMR is part of the same larger insurance family as UnitedHealthcare, but its role is usually administrative. UnitedHealthcare is often the network name families recognize, while UMR is the name that may appear on the card, claims paperwork, or member portal. For rehab admissions, that distinction matters because a treatment center may check your benefits through UMR while also looking at whether the facility participates in a UnitedHealthcare-related provider network.

How the pieces fit together

A helpful way to picture it is a three-part system. The employer builds the plan, UMR handles the day-to-day administration, and the provider network determines which doctors, therapists, and rehab centers are treated as in network.

| Part of the system | Role |

|---|---|

| Employer | Pays for the self-funded plan and chooses the benefit structure |

| UMR | Handles claims, member support, eligibility checks, and plan administration |

| UnitedHealthcare network | Provides access to participating providers and facilities |

This is why families may hear all three names during a stressful search for treatment. Each name points to a different part of the coverage process.

Why this matters for rehab

For addiction treatment, the UMR and UnitedHealthcare connection affects practical questions, not just terminology. It can influence whether a California rehab is considered in network, which services need prior authorization, and how behavioral health claims are processed.

That matters most when your loved one needs help now. Detox, residential treatment, and dual-diagnosis care often involve fast benefit checks and clear documentation. If the plan uses a broad provider network, that can widen the list of treatment options. If the plan has tighter utilization review rules, admissions may need to confirm medical necessity before care begins.

Families who want more context on the insurance brands commonly seen in employer coverage can review PIA Southern Alliance's top carriers. Families trying to sort out behavioral health details within this insurance family may also find this guide to UnitedHealthcare counseling coverage useful.

A UMR card often points to a large administrative system tied to a well-known provider network. For a family seeking luxury rehab in California, that is often good news. It usually means there is an established process for checking benefits quickly and finding out what level of addiction treatment the plan may help cover.

UMR Coverage for Substance Abuse Treatment

When a family asks what does UMR insurance stand for, the deeper question is usually this one. Will it help pay for rehab?

In many cases, the answer is yes. UMR administers plans that typically include coverage for medical services, prescription drugs, dental care, vision exams, and behavioral health services such as mental health counseling and substance abuse treatment, according to this explanation of UMR coverage and benefits.

Types of rehab services families often need to ask about

Because UMR often works with PPO-style plans, members may have access to a wide range of treatment settings. The exact benefits depend on the employer's plan, but these are the levels of care families usually need clarified during a benefits check:

- Medical detox: For withdrawal management when medical supervision is needed.

- Residential inpatient treatment: For people who need a structured, live-in environment.

- Dual-diagnosis care: For substance use and co-occurring mental health concerns treated together.

- Medication-assisted treatment: For opioid or alcohol use disorders when medications are part of the treatment plan.

- Outpatient support: For people stepping down from higher levels of care or beginning with less intensive treatment.

Why the plan details matter so much

Two members can both have UMR and still have different coverage rules. One plan may support a broader range of services at one facility. Another may require more review before residential treatment is approved. That's especially important when a family is deciding between detox, inpatient care, or outpatient treatment.

For readers trying to understand lower-acuity treatment before a residential admission decision is made, this guide to ASAM Level 1 costs and enrollment gives helpful context about one end of the treatment continuum. For those specifically asking whether a health plan may help with a live-in program, insurance coverage for inpatient rehab is a practical next read.

A realistic example

A working adult may have a UMR-administered plan through an employer and need immediate help for alcohol dependence along with anxiety symptoms. The family might assume the card only covers general medical visits. In reality, the plan may include behavioral health and substance abuse treatment, but admission depends on verifying the exact level of care, network status, and authorization requirements.

That's why families shouldn't stop at the initials on the card. UMR often opens the door to treatment. The key is confirming what the specific plan allows and moving quickly once the benefits are clear.

How to Verify Your UMR Benefits for Rehab

Once a family understands what UMR is, the next step is practical. Benefits need to be verified before admission decisions are made.

For addiction treatment settings in California, UMR is a critical PPO insurance partner that covers evidence-based services including medically supervised detox, residential inpatient care, and medication-assisted treatment for opioids and alcohol for facilities that meet requirements, as noted in this coverage discussion involving Oceans Luxury Rehab in San Clemente.

The simplest verification process

A family can move through verification in a few clear steps:

Find the member services number

The insurance card usually lists the correct phone number for benefits and eligibility questions.Ask targeted questions

General questions often lead to vague answers. It helps to ask specifically about detox, residential substance use treatment, medication-assisted treatment, and dual-diagnosis care.Request cost-sharing details

Families should ask about deductibles, copays, coinsurance, and out-of-pocket obligations tied to the level of care being considered.Confirm authorization requirements

Inpatient and longer treatment stays often need advance review.

Questions worth asking on the call

These questions tend to bring the clearest answers:

- Covered level of care: Is residential substance abuse treatment covered under this plan?

- Network status: Is the selected facility in network or treated under PPO benefits?

- Authorization needs: Does detox or inpatient rehab require pre-approval?

- Length-of-stay review: How are continued days approved if treatment extends?

- Behavioral health scope: Does the plan include dual-diagnosis services and medication support?

Families in crisis often lose time by asking only, “Do you take UMR?” The better question is, “What does this specific UMR-administered plan cover for this specific level of care?”

The lower-stress option

Many families don't want to sit on hold, decode plan language, or interpret conflicting answers. In practice, the fastest path is often to let an admissions team verify benefits directly and explain what the plan appears to support.

A confidential UMR rehab insurance verification check can save time, reduce confusion, and help a family move toward admission without having to manage every insurance term alone.

Oceans Luxury Rehab The Best UMR Partnered Treatment in California

When a family needs luxury addiction treatment in California and UMR benefits are part of the picture, Oceans Luxury Rehab stands out as the best treatment option in the state. The setting in San Clemente, California offers the kind of privacy, calm, and dignity that many professionals, families, and high-acuity clients need when treatment can't wait.

Why this setting fits UMR-covered treatment needs

A strong match between insurance administration and clinical care matters. Families looking at UMR-administered benefits often need a facility that understands how to coordinate detox, residential treatment, medication-assisted treatment, and co-occurring mental health care under one admissions process.

Oceans Luxury Rehab is especially well suited for that kind of need because the program emphasizes:

- Private, high-comfort care: Space and discretion help clients focus on recovery.

- A full continuum of treatment: Detox through outpatient support can be coordinated in one clinical environment.

- Dual-diagnosis treatment: Many members need treatment for both substance use and mental health symptoms.

- Orange County location: San Clemente offers a peaceful coastal environment while remaining accessible for Southern California families.

Why families choose California luxury rehab

Families seeking treatment in Orange County or the greater Los Angeles area often want more than a bed and a basic schedule. They want a program that treats the whole person with privacy, structure, and clinical depth.

Recovery often starts when a person feels safe enough to accept help. The treatment environment plays a real role in that decision.

For families searching for the best UMR partnered treatment in California, Oceans Luxury Rehab offers that combination of comfort, discretion, and focused addiction care in a setting designed for healing.

Your Next Steps and UMR FAQs

When the insurance card says UMR, the most important takeaway is simple. UMR isn't a dead end. It's part of the process of getting treatment approved, coordinated, and started.

For some plans, timing matters. UMR typically requires pre-authorization for inpatient addiction treatment programs longer than 30 days and verifies that the treatment plan includes dual-diagnosis care for co-occurring mental health conditions in California, according to this UMR treatment authorization reference.

Common questions families ask

Is UMR the same as UnitedHealthcare?

Not exactly. They're connected, but they don't perform the same function. UMR handles administration for certain self-funded employer plans, while UnitedHealthcare is the larger insurance brand many people already recognize.

Does a UMR plan cover out-of-network rehab?

It can, depending on the plan design. Some PPO arrangements offer broader flexibility than families expect, but the exact out-of-network terms need to be verified before admission.

Will detox and residential treatment both require review?

Often, yes. More intensive services commonly require eligibility confirmation and authorization review, especially when a longer inpatient stay may be needed.

What if the family doesn't know the policy details?

That's common. The member ID and the phone number on the insurance card are usually enough to begin verification.

The clearest next step

A family in distress doesn't need to master insurance language before asking for help. What matters is acting quickly, confirming benefits, and connecting the person in need with the right level of care.

If there's immediate concern about alcohol, opioids, prescription drugs, or another substance, the fastest step is to begin a confidential insurance check and admissions conversation right away.

Families who need fast, private help can reach Oceans Luxury Rehab to verify UMR benefits, clarify admission options, and take the next step toward detox or residential treatment in California. The admissions team can help make sense of the insurance details and guide a clear path into care with compassion and urgency.